Money, money, money. Always sunny. In the [fund managers’s] world – ABBA

If you have ever been inside a VC firm’s office, you’ve probably seen a few things that seem excessive. It can range from a bee apiary on the roof to meeting rooms featuring tables that seem unnecessarily long [and expensive]. Some of thoselive-edge tablesalone can cost over $ 20, 000 . Once you understand how VC firms make money, it becomes clear why firms can afford to buy those tables for their fancy offices on Sand Hill Road (home of the most expensive commercial rental space in US)

Two and Twenty

If you ask most VCs to describe their fee structure, most will say, “2 & 20 ”. That term describes a 2% management fee on committed capital and a 20% profit-sharing split as carried interest. The management fees and carried interest are fees that the Limited Partners (the institutions or people providing most of the money for the fund) agree to pay to the VC firm as compensation for finding investments and administering the fund. Like many other structural parts of VC, this standard for fees was imported from hedge funds and private equity firms.

Chris Harvey has a good list of the standard terms on a $ 50 M fund. We’ll dig into the mechanics of each the of the terms below.

Management Fees – The Two in “2 & 20 ”

The management fees are used to pay for salaries, rent, travel, marketing, software, swag (like Patagonia jackets), and events like the annual LP meeting.

The catch that many people outside of venture miss is that the management fee is chargedevery year of the fund’s life(which is usually around 10 years long). That means that a standard fund will charge 20% of the fund’s total raised capital in guaranteed fees and can only use the remaining 80% to actually invest in companies. A good rule of thumb is that for every $ 1 a LP provides, only about $ 0. 80 – $ 0. 85 will be invested.

Every time you hear about a new fund that raised a billion dollars, keep in mind that aroundtwo hundred million dollarswill go to the firm for “operational expenses and compensation”. Most funds are only actively making new investments for two to three years and for the rest of the time the fund is in maintenance mode. Do you need $ 200 M to operate a twenty person firm for four years and to keep the lights on to make follow on investments for the next six years? Not really.

These economics change when you have a smaller fund (say, under $ (M). These funds typically charge 2.5% since many of the operational costs of running a fund are somewhat fixed regardless of fund size. If you have a fund under $ 10 M, you aren’t going to be making a lot of income on management fees after accounting for fund expenses and overhead. Alternatively, some VC firms choose to front-load the management fees during the period that the fund is actually investing by charging a larger percent on the capital pulled from LPs during the first three years and then charging a correspondingly lower percent for the last seven years . We will dig into capital calls in another post, but when it comes to management fees, the fees are calculated based on the total committed amount to the fund, not just the cash that the fund already has in the bank.

After accounting for cash left aside for follow on investments (usually around half of the investable cash), VCs only end up deploying ~ 40% of the total amount of funds they raise into new investments.

Some VCs also charge their portfolio companies for legal fees that the firm incurs during the process of investment. The investment documents set a maximum amount that the firm can charge the company for legal fees. In what can only be explained as a coincidence, the actual legal fees incurred always seems to hover around just below that maximum amount. It is almost as if the lawyers have figured how this system works and how to maximize their billable hours. VCs can use the proceeds from companies to reimburse LPs for management fees. There are a few firms (like K9, Afore, and Homebrew) that havecommitted to not charge companiesfor the fund’s own legal fees in a round. VCs will argue that the company should pay since the legal and due diligence fees are shared among all the investors in the round, but it is hard to deny that the status quo is an inefficiency that legal firms have efficiently squeezed into.

Carried Interest – The Twenty in “2 & 20 ”

While guaranteed fees like management fees are nice, good VCs make the real money on their performance fees taken in the form of carried interest (known as carry).Legend has itthat the origins of carry date back to whale hunting expeditions where the crew could take a portion of the proceeds for themselves, specifically whatever they could carry off the boat after returning.

Similarly, the general partners of a VC fund are entitled to receive a percentage of the profits of their investments as carried interest (usually only of the proceeds after the VCs return the original capital contribution of the LPs).

For example, if the fund raises $ 100 M with the standard 2 & 20 fees, and turns that into three times the original capital $ (M) from $ 80 M of invested capital assuming 2% management fees). VCs are entitled to take 20% of the $ 200 M they generated for the LPs. That comes out to $ 40 M of carried interest for the VC firm, which is taxed as capital gains (and almost certainly long term capital gains since returns in venture take much longer than the three year threshold that Congress recently set for carried interest).

After accounting for Management Fees on this 3x hypothetical fund, LPs end up paying around $ 60 M in fees to a firm with only a few partners. The firm now has to divvy up the b̶o̶u̶n̶t̶y̶ well deserved performance fees among the partners. The specifics of how this is done depend on each firm. Many times the partners that brings in a deal gets a larger chunk of the carry on that deal. This unequal split & attribution issues are a root cause of the intense politics that happens within the partnership to claim credit and pound the table for your own deals. The exception is to divide carry equally among the partners involved with each fund. Some of the best firms, including Benchmark, do equally split the carry among partners.

The logistics of when VCs receive cash from exits depends on the terms and is usually modeled as a waterfall. There are two schools of thought for this calculation, namely the “American Waterfall” which favors GPs and the far more popular “European Waterfall” which favors LPs.

The “American Waterfall” where carry is distributed on a deal by deal basis and may be clawed back from VCs at the end of the fund if it doesn’t return enough capital overall. With the “European Waterfall” capital has to be returned to LPs at a fund level before carry is distributed. In this model, GPs only get carry once all of the original capital is returned to investors and any additional return requirements are met. This requirement means that VCs will not get paid carried interest until they return the fund, which could take six to eight years.

Even though VCs and LPs expect funds to 2-3x at a minimum, many VCs don’t hit this threshold, so the firm mostly just pockets the management fees .

As long as VCs can continue to raise from new funds LPs, they get another shot. Because VCs raise a new fund every two to three years, the return profiles of their old funds are not always clear. LPs are inclined to stick around with VCs for a long time, because of their own FOMO (fear of missing out) on a particularly great vintage (the year in which a fund started making investment).

For the funds with exceptional returns, the partners might be sitting on generational wealth through their carry. As of last year, Benchmark’s2011 vintage (their seventh fund) was famously sitting on about $ 13. 5 billion of returns(a value of $ 14 B on $ (M invested). There were seven partners on that fund and depending on how much carry Benchmark charged on that fund (likely 30%), each of the partners are potentially taking home about $ (M – $) M in carried interest (before taxes) as those positions exit. Those are numbers that make many traditional private equity and hedge fund managers jealous. And that’s just from one fund, VCs raise new funds every two to three years.

Once a fund reaches the end of its designated life time (10 years), it can be extended for a little bit to allow companies to exit, but VCs are pressured to get their stakes to be liquid so that they can capture the returns (and carry) as well as close out the fund to longer pay the administrative cost to keep the fund running. If their ownership stake has been written down and they don’t see an exit anytime soon (“impaired” in VC parlance), VCs may just write off the investment or sell the stock in a secondary transaction.

Bonus: “Fund Expenses”

In addition to charging LPs management fees, VCs are entitled to use some of the fund’s own capital for costs that are incurred to actually raise and administer the fund (for example the formation fees for the actual fund and certain audits ). Now you might wonder, isn’t this exactly what management fees are for? You could make that case, but VCs and LPs have an agreement (the Limited Partnership Agreement) that can spell out what can and cannot be charged to the fund) and a hard cap on organizational expenses for setting up the fund.

“But what about Fee Recycling?”

VCs reading this might dismiss their notion of them charging high fees by saying that they “recycle management fees”. What that means is that instead of immediately pocketing their management fees, a chunk (or all) of it gets to be used for investing in companies (typically in follow on rounds of existing portfolio companies).

VCs are still entitled to the same chunk of fees but they are just issuing a free loan to their LPs in exchange for hopefully getting more carry and getting the original fees back later. It aligns incentives better, but at the end of the day it is essentially just a way to get a larger effective fund size without asking for more capital from LPs. If you are a good investor, this will result in better returns for everyone, but it’s not really cutting into the fees that VCs charge, recycling merely delays those fees.

It pays to be a winner: “3 & 30 ”

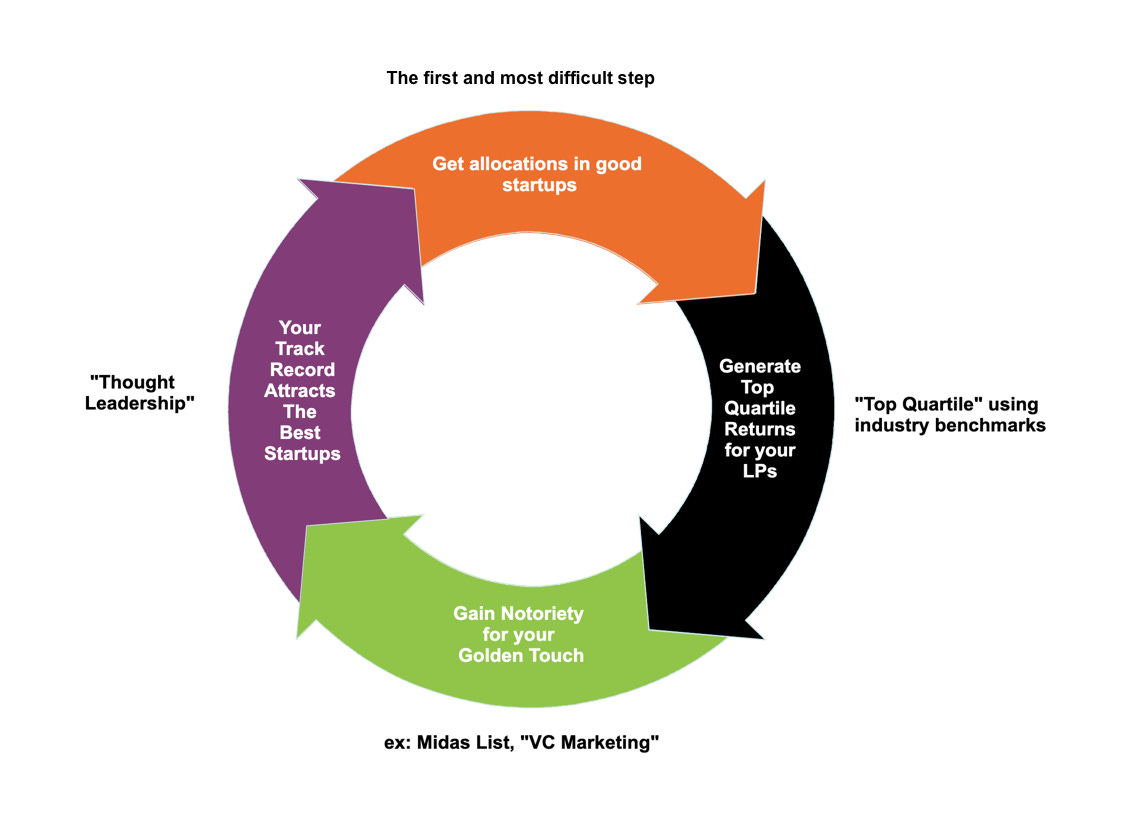

For the firms that consistently produce great returns (think Sequoia and Benchmark), LPs are constantly competing to get an allocation because those funds are likely to continue to produce good returns (because of “The Top Quartile VC Loop”).

If you’re able to get into Sequoia’s fund (which only accepts non-profit LPs) or Benchmark’s funds you aren’t going to quibble about the higher fees they charge because you can be more confident that they will have superior performance (thanks to their established reputation) and that even getting an opportunity to invest is scarce.

These top tier funds often charge a higher fee, “3 & 30 ”(3% management fee and 30% carry) or even higher but their performance justifies the fees. In venture, the best firms generate a lot of the returns, so their fees are worth it. Sequoia could charge more and still oversubscribe their funds, but they’ve decided to only accept non-profits for their LPs, which conveniently serves as a way to limit demand.

If you asked an LP to choose between Benchmark’s high fees and some third tier VC for zero fees, they’d go with Benchmark each time. For LPs that don’t have access to top tier funds, they often even pay a second level of fees to managers that pool money from LPs to invest in venture funds. These funds are called “fund of funds” and often layer an additional layer of 1 & 10 Carry. If your choice is between a third tier no name fund with mediocre results or a fund of fund that can get into good funds, the choice is clear despite the additional layer of fees.

If you want to hear about exorbitant fees, Renaissance Technologies (a hedge fund) had a fund that generated ~ 71% IRR pre-fees but would charge 5 & 44 because they couldn’t support a larger fund size (to match the returns after fees your bank would need to give you an annual interest rate of 56%).

Why don’t LPs demand lower fees?

-

“Venture is the only asset class in the world where the asset chooses the manager and not the other way around”. Finding people who can do venture well is difficult

-

LPs are understandably risk averse about changing fee structures given their obligation to responsibly allocate their institution’s capital.

-

You don’t want to develop a bad reputation with GPs who may prevent you from investing in any of their future (potentially high performing) funds.

-

Once an LP back a funds, they are inclined to almost automatically commit for a few more funds with the manager to track performance.

-

In theory, the fees won’t matter if VCs out perform the benchmark.

“2 & 20 ”” (or more) is the standard practice among many asset managers (though it is falling out of favor in other asset classes)

For a deeper look into why LPs even invest in venture, I’d recommend Scott Kupor’s latest book,Secrets of Sand Hill Road.

Carry Hurdles

LPs can sometimes insist on a certain rate of return (known as a carry hurdle) before VCs can take carry so that they can ensure they get a sufficient rate of return (around 8 – 10% per year) on their own capital before VCs start dipping their hands into the profits. If a fund is using the “American Waterfall” model for carry calculations, GPs get carry when a specific investment exits (if the return rate on that investment meets the hurdle) but if when the fund closes the overall fund level returns do not meet the hurdle, the carry that was distributed can be clawed back. If a VC happens to have used that cash to buy a mansion in the Hamptons, they probably be making a call their real estate broker.

Carry hurdles also allow VCs to charge more in carry if they outperform expectations. The math isn’t particularly interesting, but the salient point is that there are some limitations that LPs can impose on high fees and ways to charge more if the fund out performs.

Management Companies & Salaries

If you’re a partner or managing partner at a large firm ( $ 750 M AUM), you’re probably making somewhere between $ 350 k and $ 500 k in yearly compensation. It’s not a bad gig but again that’s not where the real money is. It’s in the carry (as usual) and in the ownership of the underlying management company. What goes unsaid, is that only the actual partners in the fund get any carry, associates just get a comfortable salary and the prospects of becoming a partner (at another firm obviously)

The management company for the fund is the entity that actually receives management fees. It pays out salaries and certain expenses for running the fund. Anything that’s left over is kept for the management company and is distributed to the owners of the management company as profits. Doing some napkin math on a firm with $ 1B AUM, the management company receives $ 20 M each year in management fees. After some generous assumptions, for a fund with a staff of 22, they’d spend around $ 10 M to operate the fund every year. The ~ $ 10 M of profit goes to holders of the management company (which usually comprises of a few key GPs of the fund and the founders of the firm).

As the founders of firms retire, they can continue to keep a portion of the management company and receive their chunk of profits despite not being involved in day to day operations of the new funds. When there is an acquisition of a VC firm, the actual asset being acquired is the management company and the brand. You could build a solid business solely by acquiring the GP stakes in management companies and funds; unsurprisingly, that is whatsome large firms like Goldman Sachs and Blackstone are looking to do(though mostly in the world of PE).

Being a VC is not all high salaries and nice perks though, if you are an actual carry earning partner in a fund, you do need to pony up some of your own money as part of a what’s called a “GP commit”. LPs usually require the partners to contribute 1-5% of the total fund size using their own money. This helps align incentives but also isn’t enough of the fund that VCs would be too conservative with their decisions. Typically this is usually 1-2% of the fund. So if you are raising a $ 250 M fund, the partners are expected to contribute (in aggregate) $ 2.5 M to $ 5M. If a partner doesn’t have the kind of cash to pay their commit up front, either they can get a personal loan from a bank or have the fund offset a corresponding amount of management fees in lieu of a commit. Banks frequented by VCs like SVB have specific offerings for this kind of lending among other lending products (like helping funds borrow capital to deploy ahead of an official capital call)

It might sound like being a VC is a great business, and it can be, but it’s filled with pitfalls. If your goal is “change the world” and / or “build obscene amounts of wealth”, you are probably better off building a company than becoming a VC because many VCs don’t make much money beyond their salary. to become a VC it helps to have acquired some money beforehand (to pay your GP commit among other things).

Meanwhile, for those of you hoping to score a fancy live-edge table, you will need to hope that you can manage to catch the VC firm’s office manager selling off their old tables on Craigslist when the firm upgrades to an even fancier table

Acknowledgments

Special thanks to@ ChrisHarveyEsq,@ MasonNystromand@ TurnerNovak(among others) for reviewing an early draft of this.

If you’re intere sted reviewing future drafts or have suggestions for future posts please… let me know how I can be helpful on Twitter:@ vcstarterkit

GIPHY App Key not set. Please check settings