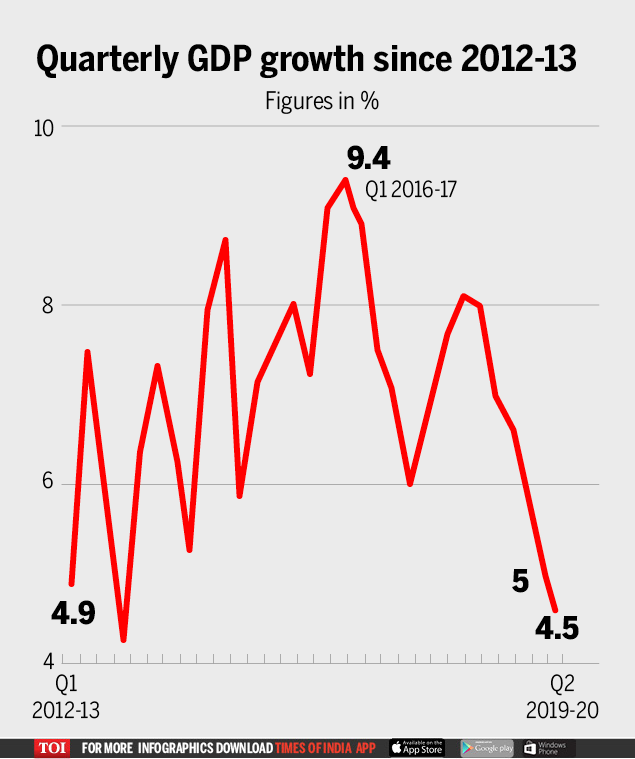

NEW DELHI: India’s gross domestic product (GDP) growth for the second quarter (July-September) slumped to 4.5 per cent from 5 per cent in the previous June quarter, government data showed on Friday. The GDP figure is a culmination of several months of downbeat figures, from weak consumer demand and private investment, to shrinking factory output and an export slump.

GDP growthstood at 7 per cent for the same quarter last year. The lowest quarterly GDP growth recorded since 2012 – 13, when the new GDP series began, was 4.3 per cent in the March quarter of 2012 – 13.

The growth dragged mainly by deceleration in manufacturing output and subdued farm sector activity. According to the data released by National Statistical Office (NSO), the gross value added (GVA) growth in the manufacturing sector contracted by 1 per cent in the second quarter of this fiscal from 6.9 per cent expansion a year ago.

Similarly, farm sector GVA growth remained subdued at 2.1 per cent, down from 4.9 per cent in the corresponding period of the previous fiscal. Construction sector GVA growth too slowed to 3.3 per cent from 8.5 per cent earlier. Mining sector growth was recorded at 0.1 per cent as against 2.2 per cent contraction a year ago.

The GDP numbers revoked strong reactions from the opposition leaders. Former Prime Minister Manmohan Singh termed the decline as “deeply worrying” while senior Congress leader Randeep Surjewala stated that the economy is “in a virtual free-fall”.

Trinamool Congress (TMC) leader Derek O’Brien took potshots at finance minister Nirmala Sitharaman over the sliding numbers and wrote on Twitter: “Lowest GDP growth in 26 quarters! No answers from FM. No wonder, full Opposition walked out of Rajya Sabha 40 minutes into the FM’s speech this week. And ministers dozed off in their seats. “

Lowest GDP growth in 26 quarters ! No answers from FM. No wonder, full Opposition walked out of Rajya Sabha 40 minut… https://t.co/QHUA7QA1ve

However, the government quickly countered the criticism from opposition leaders and stated that the economic growth “is expected to pick up from third quarter of FY 2019 – 20 “.

We take note of announcement of the rate of GDP growth. The fundamentals of Indian Economy remain strong. GDP gro… https://t.co/ (fxYk) ************************************************************ (Jh

– Ministry of Finance (@FinMinIndia)1575034224000

With the first quarter GDP growth falling to 5 per cent, the Reserve Bank of India (RBI) had sharply lowered its estimates of economic growth in the current fiscal to 6.1 per cent from its earlier estimate of 6.9 per cent, in its October policy.

Having left much of the stimulus burden to the central bank early this year, Prime Minister Narendra Modi’s government is now taking bolder steps to reverse the slump in the Indian economy. In recent months, it has slashed corporate tax rates, withdrew higher taxes on foreign investors, set up a special real-estate fund, merged state-run banks and announced the biggest privatisation drive in more than a decade. While authorities are committed to doing more, the policy room may be narrowing.

India was the world’s fastest-growing economy until last year, posting quarterly growth rates of as high as 9.4 per cent in 2016. A crisis among shadow banks – a key source of funding for small businesses and consumers – weak rural spending and a global slowdown have since conspired to bring down growth steadily.

The RBI has already cut interest rates by 135 basis points (bps) this year to the lowest since 2009, with more easing to come. It is expected to look through recent breach of it 4 per cent medium-term inflation target and deliver another rate cut in its monetary policy meet on December 5.

In another set of data released by the government, output of eight core infrastructure industries contracted by 5.8 per cent in October, indicating the severity of economic slowdown. This was attributed primarily to a steep fall in productions of coal, power and cement.

Core sector output shrinks 5.8% in October

Output of eight core infrastructure industries contracted by 5.8 per cent in October, indicating the severity of economic slowdown, according to the government data released on Friday.

The economy needs to grow at around 8 per cent to create enough jobs for its millions of young people joining the labor force each year.

Some economists believe that with persistently tight domestic credit and weak corporate profits, India’s recovery could be delayed and the pick-up would remain below potential.

The unemployment rate in October rose to 8.5 per cent, its highest since August 2016, according to the Center for Monitoring Indian Economy (CMIE), though the government estimates that urban unemployment declined.

Two days ago, in a parliamentary debate on economic slowdown, finance minister Nirmala Sitharaman said, “Every step is being taken in the interest of the country. Looking at the economy in discerning view, you see that growth may have come down but it is not recession yet, it won’t be recession ever. ” She added that steps taken by the government post Budget have started bearing fruits and some sectors such as automobiles have shown signs of recovery.

GDP dips to a six-year low: What does it mean?

09: 34

(With agency inputs)

GIPHY App Key not set. Please check settings